With the permission of a client, I recorded our conversation. He had questions on RRSPs and how they can help him in the short term and further down the line. The questions he had were great because I get these questions all the time and I thought it would be a good idea to share them with you in hopes they would help.

This is how it went:

A Client's RRSP Questions

Paul: Hi Jay. Thanks a lot for taking the time to jump on a call with me. As you know I am scratching my head a little with the thought of RRSPs and what I need to be doing with them.

Jay: Of course. Sometimes RRSPs and how they work can be a little confusing, how can I help?

Paul: Well, I keep hearing that I should be making a lump sum RRSP contribution before the deadline, which is March 1st correct?

Jay: That’s right, the deadline is March 1st. You have the first 60 days in the calendar year to help the previous years tax return.

Paul: Ok got it. So how does me making a lump sum contribution help me in the short term?

Jay: No matter where a person is on the road to retirement, an RRSP contribution is a great short term strategy to help lower your taxable income in a calendar year. Meaning, you either lower your tax owing or you increase your tax return. However, RRSP’s are typically considered a long term strategy to help one personally save to enhance their retirement lifestyle.

Paul: So would you be able to break it down for me with a fictional round number that’s easy to understand? Let’s use a round number of 100,000. If someone makes $100,000 per year, what are they taxed, what happens when they make a lump sum or even monthly contributions throughout the year, how do they help?

Jay: Let me share my screen with you Paul so you can have a visual as well;

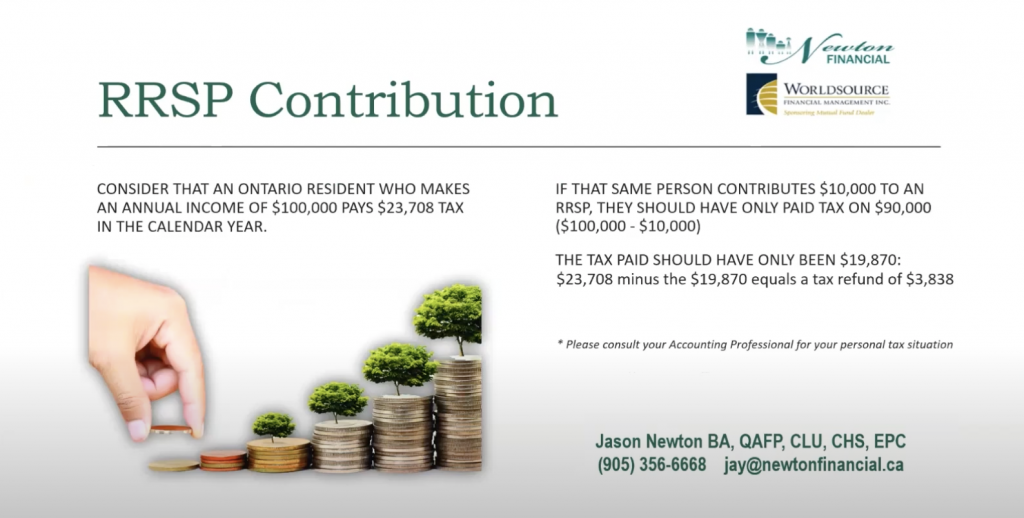

If a Person Makes $100,000 in Ontario

They should be taxed approximately $23,708 in the calendar year

If that person contributes $10,000 to an RRSP

They should have only paid $19,870 in tax (not $23,708)

This means if they made that $10,000 RRSP lump sum contribution or through regular contributions during the year they should have paid $3,838 less in taxes and enhance their tax return by $3,838.

Paul: Ok, so this person should have only paid taxes on $90,000 instead of the $100,000 thus helping their tax return with the RRSP contribution.

Jay: Correct! This individual should only pay $19,870 instead of the $23,708.

This now provides a tax return refund of $3,838. That is how it helps in the short term.

Paul, each individual is different and would have different tax deductions. I would always recommend they seek advice of a licensed accountant for their official tax balances.

Paul: Thanks, that makes it crystal clear.

Jay: You’re welcome Paul. Thank you for your time. All the best.

If you have any questions or would like to make a contribution to your RRSPs before March 1st, Please don’t hesitate to CONTACT US.